The Great American Restaurant Squeeze: How Red Lobster's Collapse Reveals the Death of the Middle

Casual dining chains are vanishing as consumers split between $5 burritos and $200 tasting menus, leaving nowhere for the $20 dinner to hide.

Red Lobster's bankruptcy in 2024 wasn't just about endless shrimp promotions gone wrong. When the 550-location chain shed 130 restaurants and warned of more closures to come, it crystallized a brutal truth: American dining has split into two worlds, and there's no profitable middle ground left.

The numbers tell a stark story. In 2024, casual dining sales dropped 0.9% while fast-casual chains grew 0.6% and fast-food expanded 1%. More telling: when casual dining restaurants close, fast-food and fast-casual concepts quickly move into their spaces. The middle market isn't just struggling. It's being systematically replaced.

The $15 Trap: Why Mid-Price Dining Can't Compete

Casual dining chains face an impossible equation. They can't match the speed and value of Chipotle's $12 burrito bowl or Raising Cane's $8 chicken combo. Yet they lack the experience and perceived quality of fine dining establishments charging $60 per entree.

Red Lobster exemplifies this squeeze perfectly. Their signature dishes hover around $20-25, requiring table service, longer wait times, and higher labor costs than fast-casual alternatives. Meanwhile, consumers increasingly view a $25 restaurant meal as either overpriced fast food or underwhelming fine dining.

The financial pressure is relentless. Commercial lease increases hit Red Lobster particularly hard because the chain was already carrying debt from private equity ownership changes. Golden Gate Capital had loaded the company with obligations before selling to Thai Union, leaving the seafood chain vulnerable when costs spiked.

This debt burden isn't unique to Red Lobster. More than a dozen casual dining chains filed for bankruptcy in 2024, suggesting systematic rather than isolated problems.

"Companies are far more interested in selling brands than in buying them," according to Restaurant Business analysis of recent consolidation trends.

The Fast-Casual Revolution: Speed Without Sacrifice

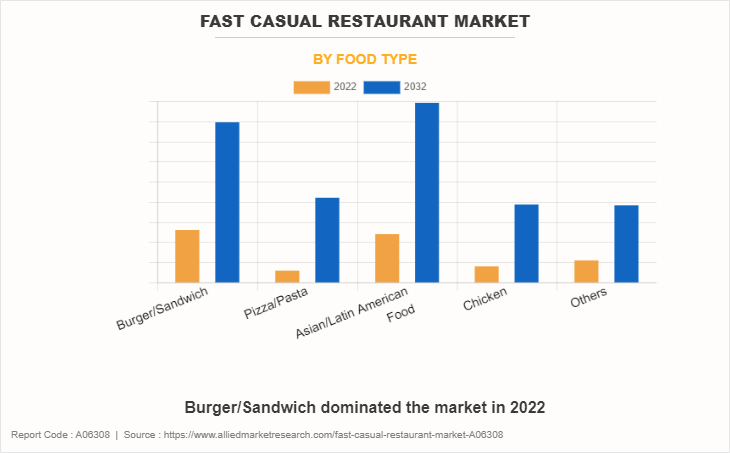

Fast-casual dining market size reached $203.64 million in 2026 and is projected to hit $246.67 million by 2035. This 21% growth over nine years reflects consumers' preference for quick, customizable meals that feel healthier and more authentic than traditional fast food.

Chipotle perfected the formula: visible food preparation, customizable options, and price points that make a $12 meal feel reasonable. Cava brings Mediterranean flavors to the same model. These chains deliver perceived quality and speed that casual dining simply cannot match.

The shift becomes clear in consumer behavior data. Technomic research shows 8.1% of recent quick-service occasions were taken from fast-casual restaurants, compared to 6.9% the year prior. Fast-casual isn't just growing. It's actively stealing market share from both ends of the spectrum.

Yet even fast-casual faces headwinds. The 2026 Restaurant Outlook warns that fast-casual operators must "redouble efforts to deliver clear, consistent value" as consumers become more selective and value-focused competitors emerge.

Premiumization: When $200 Becomes the New $50

At the opposite extreme, fine dining has embraced radical premiumization. The global fine dining market, dominated by independent restaurants in Europe and high-end chains in the Americas, caters to consumers willing to pay exponentially more for perceived quality and experience.

This trend, dubbed "premiumization" by industry analysts, sees younger consumers demanding transparency and authenticity from food brands. They'll pay $200 for a tasting menu at a chef-driven restaurant while rejecting a $25 Red Lobster dinner as inauthentic.

The premiumization phenomenon extends beyond restaurants to food and beverage brands generally. According to Bain & Company, insurgent premium brands are challenging incumbent food companies in both directions: losing market share to private labels on price and to premium products on quality.

Restaurant chains caught in the middle struggle to justify their positioning. Why pay $22 for Red Lobster's fish and chips when you can get similar food for $9 at a pub or a transformative dining experience for $80 at a chef-owned establishment?

The Death of Loyalty: Why Chain Dining Lost Its Appeal

Casual dining chains built their business model on predictable experiences and family-friendly pricing. But consumer preferences have fundamentally shifted away from these values.

Modern diners prioritize either convenience and value (fast-casual) or unique experiences (fine dining). The reliable but unremarkable experience that chains like Red Lobster, TGI Friday's, and Hooters provide no longer resonates with key demographics.

Social media amplifies this shift. Consumers share photos of their $15 Sweetgreen salad or their $150 omakase dinner. Nobody posts about their Tuesday night at Applebee's.

"For restaurant brands, value in 2026 needs to be redefined against a more selective consumer base," warns the latest Restaurant Outlook.

The consolidation data supports this trend. Major restaurant groups are selling brands rather than acquiring them. Jack in the Box is divesting Del Taco. Restaurant Brands International focuses on fixing existing chains rather than expanding portfolios.

What Comes Next: The New Restaurant Reality

Red Lobster's CEO has indicated the chain may need to close additional restaurants beyond the 130 shuttered during bankruptcy. This isn't just operational optimization. It's recognition that demand for mid-market casual dining has permanently contracted.

The surviving casual dining chains will likely need to choose a side: either race to the bottom with value pricing and faster service, or move upmarket with higher-quality ingredients and elevated experiences.

Smart growth strategies for mid-market restaurants now focus on margin preservation over expansion. The KPMG poll of senior restaurant executives shows growth ambitions, but tempered by inflation concerns and cost pressures.

Some concepts may survive by embracing hybrid models. Panera combines fast-casual service with cafe ambiance. Shake Shack elevates fast-food ingredients and presentation. These brands succeed by clearly positioning themselves within one segment rather than straddling the middle.

The broader implication extends beyond restaurants. Red Lobster's collapse signals the end of middle-market positioning across American retail and hospitality. Consumers increasingly choose between value and luxury, leaving little room for the formerly profitable middle ground.

For the restaurant industry, this means accepting a new reality: the great American squeeze has arrived, and the middle is no longer a safe place to do business.