First Mining Gold: The 5-Million-Ounce Bet That Could Define Canadian Junior Mining

Why this Ontario-focused company's Springpole project represents either a generational opportunity or a cautionary tale for gold investors.

While most Canadian junior gold miners chase trendy jurisdictions in Africa or Latin America, First Mining Gold (TSX: FF, OTCQX: FFMGF) has made a contrarian bet that could pay off spectacularly. The Vancouver-based company sits on what might be Canada's next major gold mine: the Springpole Gold Project in northwestern Ontario, containing 5.19 million ounces of measured and indicated gold resources.

The question facing investors isn't whether Springpole contains enough gold to matter. It's whether First Mining can navigate the regulatory maze, secure the $1.8 billion in capital required, and actually turn those ounces into cash flow. With a federal environmental assessment decision expected in Q1-Q2 2026, the company stands at a critical inflection point.

The Springpole Gamble: Massive Scale Meets Regulatory Reality

First Mining's updated pre-feasibility study, filed December 1, 2025, paints an ambitious picture. The company envisions producing an average of 327,000 ounces of gold annually over a 16-year mine life, generating $8.2 billion in after-tax net present value at current gold prices.

Those numbers would place Springpole among Canada's top-tier gold operations, comparable to established mines like Goldcorp's Red Lake complex. But the path from feasibility study to first gold pour remains treacherous for junior miners.

The project's economics look compelling on paper. At a gold price of $2,400 per ounce, Springpole shows an internal rate of return of 19.4% and a payback period of 4.8 years. Strip away the financial modeling, though, and you find a company burning through cash while waiting for regulatory approval.

First Mining reported a net loss of $46.4 million for the nine months ended September 30, 2025, compared to $34.5 million in the same period of 2024. The company had $15.8 million in cash and equivalents as of Q3 2025, enough to fund operations into 2026 but insufficient for major construction.

Beyond the Flagship: A Portfolio Play With Hidden Value

While Springpole dominates the investment thesis, First Mining controls a broader portfolio of gold projects across eastern Canada that could provide optionality as gold prices remain elevated.

The company's Duparquet project in Quebec sits on the prolific Destor-Porcupine fault zone, the same geological structure that hosts some of Canada's most famous gold mines. The Cameron project in northwestern Ontario adds another 830,000 ounces of inferred resources to the portfolio.

"We've assembled one of the largest pure-play Canadian gold development stories, with projects spanning multiple provinces and geological settings," management noted in recent investor presentations.

This geographic diversification matters more than most investors realize. Canada's federal and provincial regulatory systems can vary significantly, giving First Mining multiple pathways to development if one project encounters delays.

The company has also maintained optionality through strategic partnerships and spin-outs, including interests in Treasury Metals and PC Gold, allowing shareholders to benefit from broader regional exploration success.

Management Track Record: Experience Meets Execution Challenges

First Mining's leadership team brings legitimate mining industry experience, with CEO Dan Wilton previously serving as COO at Goldcorp during its acquisition of several major gold assets. The technical team includes geologists and engineers who have worked on successful mine developments across Canada.

But experience doesn't guarantee execution, particularly for junior miners facing billion-dollar capital requirements. The company has yet to demonstrate its ability to manage a construction project of Springpole's scale and complexity.

Recent management moves suggest the team recognizes these challenges. The company has brought in experienced mine builders and financing specialists, signaling preparation for the next phase of development.

Stock-based compensation of $1.2 million over nine months shows management remains committed, though some investors question whether executive incentives align properly with shareholder returns during the pre-production phase.

The 2026 Catalyst: Environmental Approval as Make-or-Break Moment

Everything for First Mining hinges on receiving federal environmental assessment approval for Springpole in Q1-Q2 2026. This isn't just another regulatory hurdle, it's the difference between a development-stage gold company and a collection of interesting geology reports.

The environmental review process has already consumed more than four years, with First Mining submitting its Environmental Assessment/Environmental Impact Statement in November 2024. The company has worked extensively with local First Nations communities, signing impact benefit agreements that should smooth the approval process.

Canadian mining companies have generally seen improved success rates with federal environmental approvals over the past two years, as the government seeks to balance environmental protection with domestic resource development. Springpole's location in an established mining region, rather than pristine wilderness, works in its favor.

But regulatory approval alone won't guarantee success. First Mining will still need to raise $1.8 billion in construction financing, a challenging proposition for any junior miner regardless of project quality.

Valuation and Investment Outlook: Asymmetric Risk-Reward

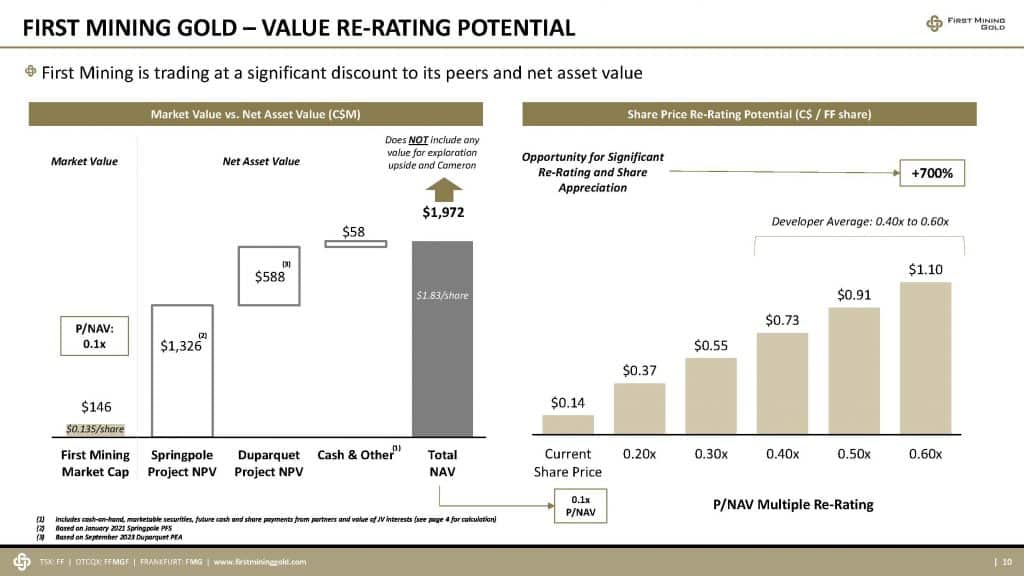

Trading around $0.43 per share on the OTC markets, First Mining Gold offers classic junior mining risk-reward dynamics amplified by Springpole's enormous scale. National Bank Financial maintains an "Outperform" rating with a target price of $1.18, implying potential upside of 174%.

Analyst consensus suggests the stock could reach similar levels if environmental approval comes through, though such predictions assume successful financing and construction execution. The company's current enterprise value of approximately $280 million represents less than $60 per ounce of gold resources, a significant discount to producing miners.

Comparisons to other Canadian junior gold miners highlight both the opportunity and risk. Companies like Treasury Metals and Wesdome Gold Mines trade at higher valuations per ounce, but with smaller resource bases and different risk profiles.

The investment case ultimately comes down to probability-weighted outcomes. If Springpole receives approval and First Mining successfully finances construction, the stock could deliver multi-bagger returns. If regulatory delays continue or financing proves elusive, shareholders face potential dilution or stagnation.

For investors willing to accept binary risk, First Mining represents one of the purest plays on Canadian gold development at a time when domestic mining assets are increasingly valuable.

The company's cash position provides runway through 2026, but additional financing will be required regardless of Springpole's regulatory outcome. Management has indicated plans for strategic partnerships or joint ventures to reduce dilution, though specifics remain limited.

Investors should watch for three key catalysts over the next 18 months: federal environmental approval, construction financing arrangements, and potential strategic partnerships. Success on all three fronts could transform First Mining from a speculative junior into a legitimate gold development story. Failure on any front will likely send the stock back to the drawing board.

In a market where proven gold deposits are increasingly scarce and expensive to acquire, First Mining's 5.19-million-ounce resource base offers compelling value for patient investors. The question is whether patience will be rewarded with execution or tested by continued delays.