Applied Digital's $2.6 Billion Debt Time Bomb: When AI Hype Meets Financial Reality

Despite $16 billion in contracts and 250% revenue growth, the math reveals a company that can't service its debt from operations.

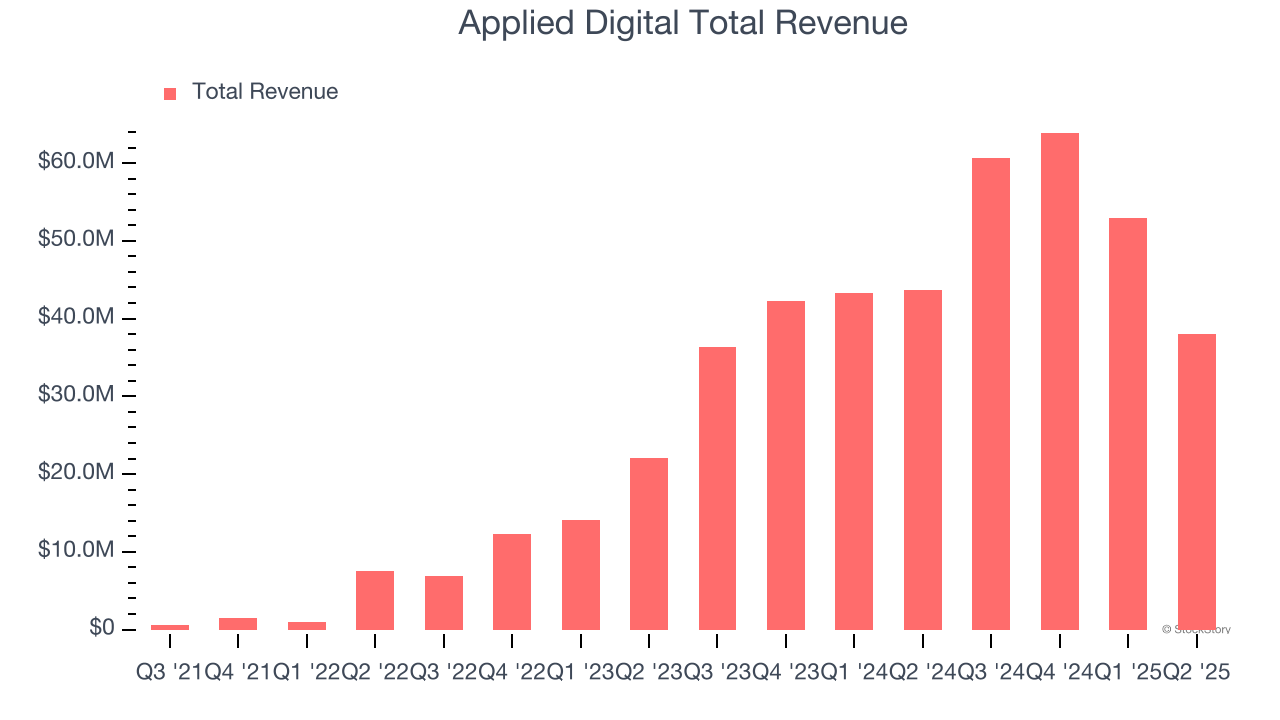

While Wall Street celebrates Applied Digital's meteoric 250% revenue growth and $16 billion contract backlog, a deeper look at the numbers reveals a troubling reality: the company borrowed $1.91 billion in just three months, pushing total debt to $2.6 billion. The annual interest expense alone now exceeds $240 million, yet projected free cash flows struggle to reach $28 million. This isn't sustainable growth—it's financial engineering on borrowed time.

The Debt Explosion That Changes Everything

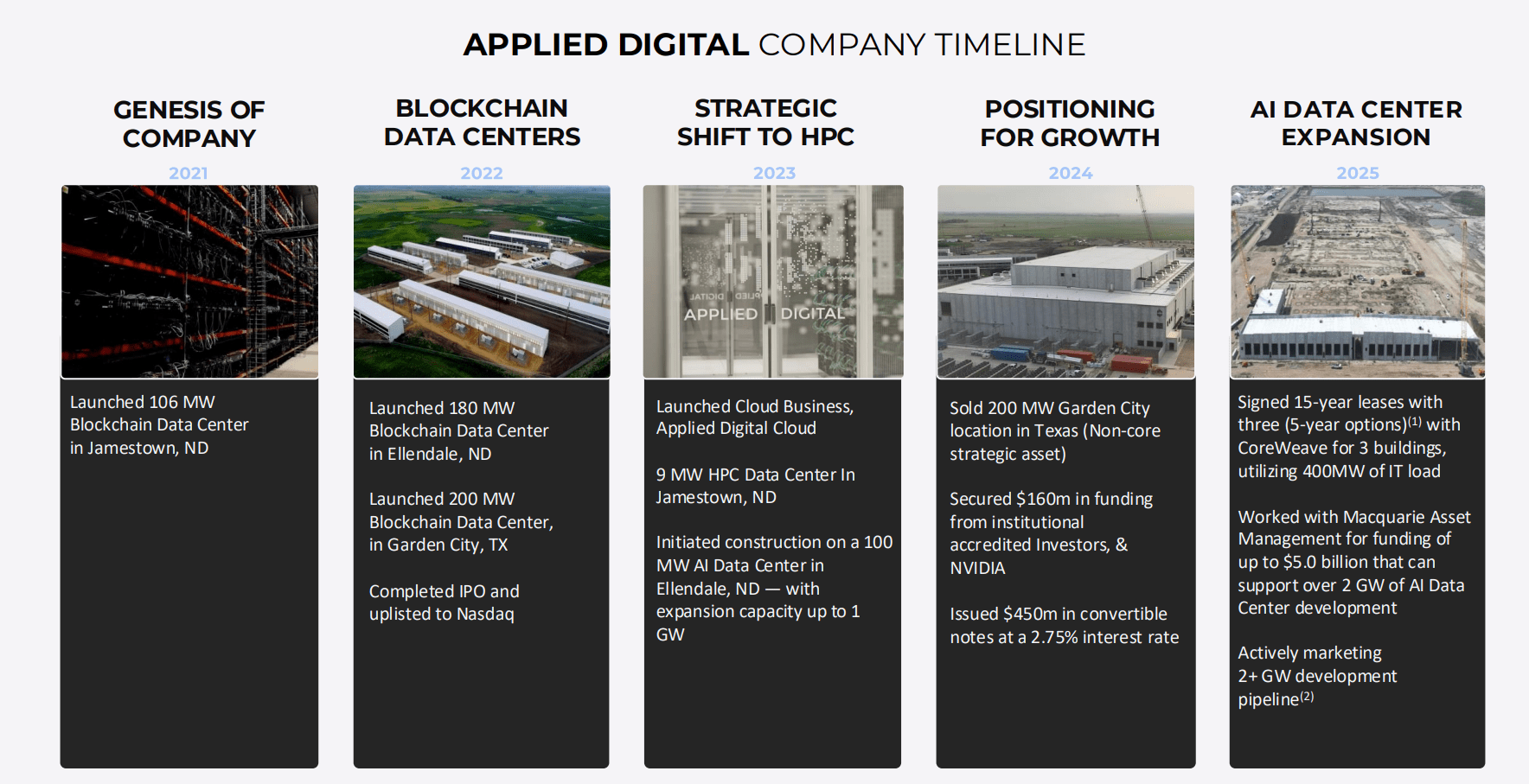

Between August and November 2025, Applied Digital executed one of the most dramatic debt expansions in recent corporate history. Total debt skyrocketed from $687.3 million to $2.6 billion—a staggering 278% increase in just one quarter. This $1.91 billion borrowing binge was designed to fund the company's Polaris Forge data centers in North Dakota.

The company's 9.25% senior notes carry an annual interest burden of approximately $240 million. For context, Applied Digital's entire trailing twelve-month revenue is only $370.1 million. The company is paying nearly 65 cents in interest for every dollar it generates in revenue.

Cash position improved to $2.3 billion, bringing net debt to $300 million. But this temporary cash cushion masks the fundamental problem: the company must generate enough operating cash flow to service massive debt while funding ongoing operations and capital expenditures.

The math is unforgiving: $240 million in annual interest costs against projected free cash flows of $10-28 million annually. The debt service requirements exceed operational cash generation by nearly ten times.

CoreWeave Dependency: A Single Point of Failure

Applied Digital's $16 billion contract backlog sounds impressive until you examine the customer concentration. CoreWeave represents $11 billion of that total—68% of all contracted revenue tied to a single, highly leveraged customer that remains unprofitable.

CoreWeave itself raised $1.1 billion in debt financing earlier this year, suggesting the AI infrastructure buildout relies heavily on borrowed capital throughout the ecosystem. If CoreWeave faces financial distress, Applied Digital loses more than two-thirds of its revenue pipeline instantly.

The lease agreements include construction milestone requirements. Missing deadlines could trigger early termination clauses, allowing CoreWeave to walk away from billions in future commitments. In a capital-intensive business where timing is everything, execution risk becomes existential risk.

Valuation Disconnect: Trading Like Tomorrow's Winner

Applied Digital trades at a 19.0x price-to-sales ratio while established data center REITs like Digital Realty Trust and Equinix trade at 10.1x and 9.9x respectively. This 90% premium assumes Applied Digital will not only match but exceed the profitability and operational efficiency of mature, proven competitors.

The current market capitalization of $7.03 billion values the company at more than 18 times trailing revenue. For comparison, Microsoft trades at 13x revenue despite generating 35% net margins and throwing off billions in free cash flow annually.

Even optimistic projections struggle to justify current valuations. Assuming the company reaches $1.1 billion in revenue by 2030 with best-in-class 30% EBITDA margins, discounted cash flow analysis still produces negative equity value after accounting for debt service requirements.

The Mathematical Impossibility

A detailed DCF analysis reveals the core problem. Base case assumptions include revenue growing to $1.1 billion by 2030, EBITDA margins reaching 30%, and capital expenditures consuming 20% of revenue. Using a 12% weighted average cost of capital to reflect execution and refinancing risks, the present value of five-year free cash flows totals just $67 million.

Adding terminal value brings enterprise value to $235 million. Subtract the $300 million net debt position, and equity value becomes negative $65 million. The intrinsic value per share calculates to negative $0.23 versus the current price of $25.14.

Sensitivity analysis shows even with generous assumptions—10% discount rates and 4% terminal growth—intrinsic value reaches only $0.24 per share. The gap between mathematical reality and market pricing exceeds 10,000%.

Every scenario analysis produces the same result: debt service costs consume all available cash flow, leaving equity holders with nothing but promises and potential.

The AI Infrastructure Mirage

Applied Digital benefits from the broader artificial intelligence narrative driving speculative investment across tech sectors. The company positions itself as a pure-play on AI infrastructure demand, promising exposure to the computing revolution without the complexity of chip design or software development.

This positioning commands premium valuations during bull markets but creates vulnerability during periods of rational analysis. Unlike established data center operators with diversified customer bases and proven cash generation, Applied Digital remains a development-stage company burning cash while building infrastructure.

The AI infrastructure thesis assumes sustained demand growth and pricing power. Both remain uncertain as hyperscalers develop internal capabilities and alternative suppliers emerge. Technology shifts in chip architecture could strand current investments, while competition from established REITs with cheaper capital costs threatens pricing assumptions.

Risk-Reward Analysis Points to Danger

Probability-weighted scenarios reveal asymmetric downside risk. The bear case assigns 50% probability to debt restructuring or bankruptcy, resulting in $0-5 per share value. Base case scenarios, with 35% probability, assume the company struggles with debt service while maintaining operations, supporting $5-15 valuations.

Only the bull case, with 15% probability, assumes perfect execution and CoreWeave's continued success, potentially driving shares to $30-40. The expected value calculation produces $8-12 per share, implying 60-70% downside from current levels.

The asymmetric risk profile reflects the binary nature of highly leveraged growth stories. Success requires everything going right simultaneously: on-time construction, customer financial health, successful refinancing, and sustained AI demand growth. Failure in any single area could trigger cascade effects given the debt burden.

Better risk-adjusted opportunities exist in established data center REITs trading at reasonable valuations with diversified revenue streams and proven cash generation capabilities. For pure AI exposure, direct investments in chip companies or software providers offer upside potential without Applied Digital's execution and financial risks.

The numbers don't lie, even when the narrative sounds compelling. Applied Digital represents speculation masquerading as investment, with debt service requirements that make current equity valuations mathematically impossible to justify. Sometimes the most important calculation is the one that tells you to walk away.