Applied Digital's $16 Billion Gamble: Why This AI Data Center Darling Is a House of Cards

Despite explosive growth and massive contracts, APLD's dependence on one overleveraged customer makes it a dangerous bet for investors.

When Applied Digital's stock price collapsed 10.5% in a single day, dropping to $25.14 from its $42 highs, most investors focused on the immediate trigger: Nvidia's complete exit from its 7.7 million share position. But the real story isn't about what Nvidia sold. It's about what Applied Digital built: a $7 billion company that depends on a single customer for 68% of its revenue, funded by debt that exploded from $44 million to $2.6 billion in just 18 months.

The CoreWeave Dependency That Should Terrify Investors

Applied Digital's business model sounds compelling on paper. The company builds AI-first data centers with extreme power density, cramming 100+ kilowatts per rack compared to the 15-20 kilowatts of traditional facilities. This specialization landed them $16 billion in contracted revenue over 15 years, a figure that dwarfs their current $7 billion market cap.

The problem lies in the details of those contracts.

CoreWeave, an AI cloud computing company, accounts for $11 billion of that $16 billion backlog. That's 68% of Applied Digital's future revenue tied to a single customer that is itself burning cash and heavily leveraged. CoreWeave projects losses of $211 billion through 2030 as it competes with OpenAI and other AI giants, raising serious questions about its ability to honor long-term commitments.

Even more concerning: the lease terms allow CoreWeave to walk away penalty-free if Applied Digital misses construction milestones. In an industry where complex data center builds routinely face delays, this clause transforms Applied Digital from a infrastructure provider into a hostage of its own construction schedule.

When 68% of your revenue depends on one customer who can terminate contracts without penalty, you're not running a business. You're placing a $7 billion bet on perfect execution.

A Debt Mountain Built on Shaky Ground

Applied Digital's aggressive expansion required equally aggressive financing. The company's debt exploded from a manageable $44 million in Q1 2024 to a staggering $2.6 billion by November 2025. This debt-to-equity ratio of over 125% would be dangerous for any company, but it's particularly risky for one dependent on flawless construction execution.

The recent $2.15 billion in secured notes carries a hefty 9.25% interest rate, reflecting the market's perception of the company's risk profile. While Applied Digital maintains a $2.3 billion cash position from recent raises, this war chest evaporates quickly when building data centers that cost hundreds of millions each.

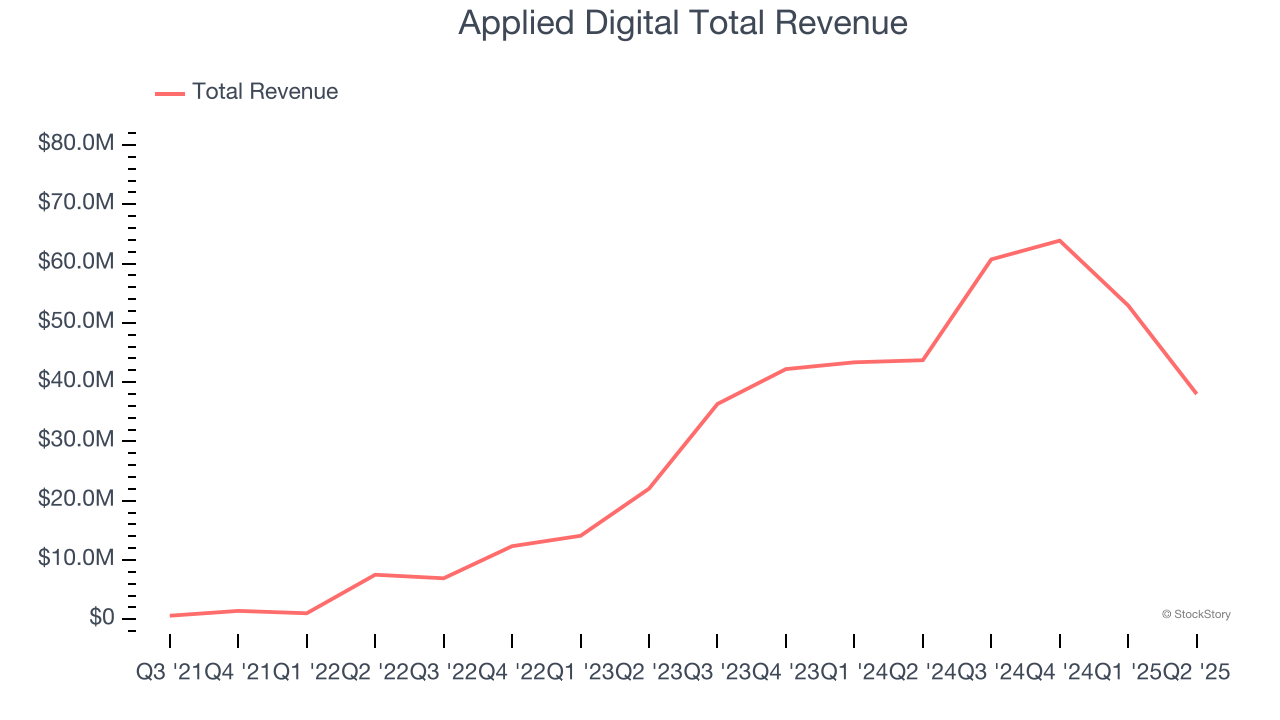

The math becomes uncomfortable when you consider refinancing risk. If market sentiment turns negative or construction delays emerge, Applied Digital could face a liquidity crunch just as it needs capital most. The company posted a $125 million annual loss despite 250% revenue growth to $126.6 million in Q2 FY26, meaning profitability remains a distant goal even as debt service costs mount.

Nvidia's Exit: The Canary in the Coal Mine

Nvidia's complete liquidation of its Applied Digital stake sent shockwaves through the AI infrastructure sector. The chipmaker's exit wasn't subtle—it sold all 7.7 million shares, signaling either a fundamental disagreement with Applied Digital's strategy or concerns about execution risk.

This matters because Nvidia has unparalleled visibility into AI infrastructure demand. The company's GPUs power the data centers Applied Digital builds, making Nvidia's vote of no confidence particularly damaging. The 8% stock drop following the exit announcement suggests other institutional investors share these concerns.

The timing compounds the problem. Nvidia's exit coincided with broader questions about AI infrastructure investment returns and the sustainability of current buildout rates. If the industry leader is stepping back, individual investors should ask why they're stepping forward.

Valuation Disconnect in a Reality Check Market

Applied Digital trades at 26 times sales, a premium that assumes flawless execution and unlimited growth potential. Compare this to established data center REITs trading at 6-11 times sales with diversified customer bases, proven operations, and sustainable dividend yields.

A DCF analysis using conservative assumptions suggests an intrinsic value range of $15-35 per share, placing the current $25.14 price in the middle of fair value territory. But this assumes Applied Digital achieves 35% EBITDA margins when mature, successfully diversifies its customer base, and avoids major construction delays—a combination of outcomes that history suggests is unlikely.

The risk-reward profile looks unfavorable: potential 100% upside if everything goes perfectly versus 60% downside if major problems emerge. For a company with this much execution risk and customer concentration, that's an asymmetric bet in the wrong direction.

The Coming Reality Check

Applied Digital operates in a market experiencing unprecedented demand for AI compute power, but that demand won't last forever at current growth rates. The company's centralized data center model assumes AI workloads will remain concentrated in massive facilities rather than distributed across edge locations—a bet that may not age well as the technology evolves.

Competition adds another layer of concern. Established players like Digital Realty Trust and Equinix have cheaper capital, proven operations, and diversified customer relationships. They're rapidly adding AI-optimized capacity without the leverage and customer concentration risks that plague Applied Digital.

In a market where execution risk meets financial leverage meets customer concentration, Applied Digital represents everything that can go wrong with growth-at-any-cost investing.

The company's Q3 earnings showed revenue declining 17% to $52.92 million, a reminder that growth in the AI infrastructure space isn't guaranteed even with massive contracted backlogs. Construction delays, customer financing issues, or technology shifts could quickly transform today's growth story into tomorrow's cautionary tale.

For investors seeking AI exposure, better opportunities exist in established data center operators with diversified revenue streams or direct chip plays with clearer competitive advantages. Applied Digital's combination of extreme leverage, customer concentration, and execution risk makes it unsuitable for most portfolios—regardless of the AI boom's continuation.