The $30 Billion OpenAI Deal Isn't About Money—It's About Control

Nvidia's scaled-back investment reveals how AI's biggest players are quietly choking out competition while building unbreakable monopolies.

When Nvidia announced it was finalizing a $30 billion investment in OpenAI—down from the initially promised $100 billion—most analysts focused on the reduced dollar amount. They missed the real story. This isn't a company cutting back on AI. It's a strategic masterclass in market control disguised as partnership friction.

The supposed "stalling" of the original deal, reportedly due to CEO Jensen Huang's private criticisms of OpenAI, creates perfect cover for what's actually happening: the systematic elimination of AI competition through infrastructure dependency. While everyone debates whether this represents cooling enthusiasm for AI, the real question is whether we're witnessing the birth of an unbreakable duopoly.

The Circular Money Machine That's Rigging the Game

Here's what the headlines won't tell you about Nvidia's investment strategy. The company isn't just writing checks to OpenAI—it's creating a circular financing system that guarantees its own dominance while appearing to support competition.

OpenAI uses Nvidia's investment to buy Nvidia's chips. Those chip sales boost Nvidia's revenue, which justifies higher valuations and more investment capital. That capital flows back into more OpenAI investments, creating an endless loop where Nvidia's money never actually leaves the ecosystem—it just changes hands while tightening the noose around competitors.

"The critical question for founders has evolved beyond 'can you build a better product?' to 'Can you build a moat so deep that even a platform update can't erode it?'"

Fortune analysts are already drawing parallels to previous tech bubbles, but they're missing the sophistication of this setup. Unlike the dot-com crash, where money disappeared into failed business models, this circular system creates real assets—data centers, chips, and infrastructure—that become increasingly impossible for outsiders to replicate.

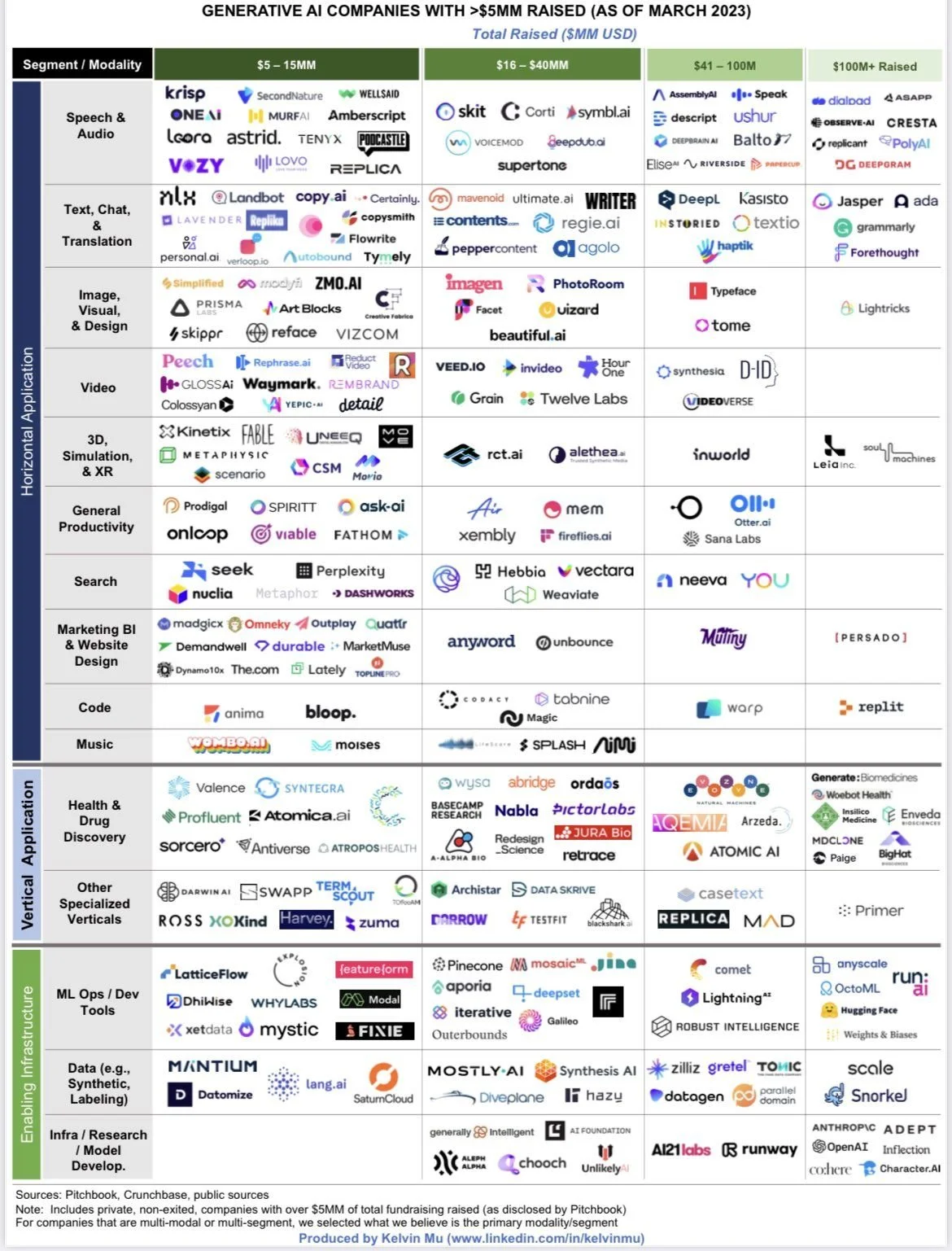

The numbers tell the story. AI companies pulled in nearly $60 billion globally in Q1 2024 alone—more than half of all venture funding that quarter. But here's the catch: most of that funding flows directly back to the same handful of infrastructure providers.

The 10-Gigawatt Fortress That Locks Out Innovation

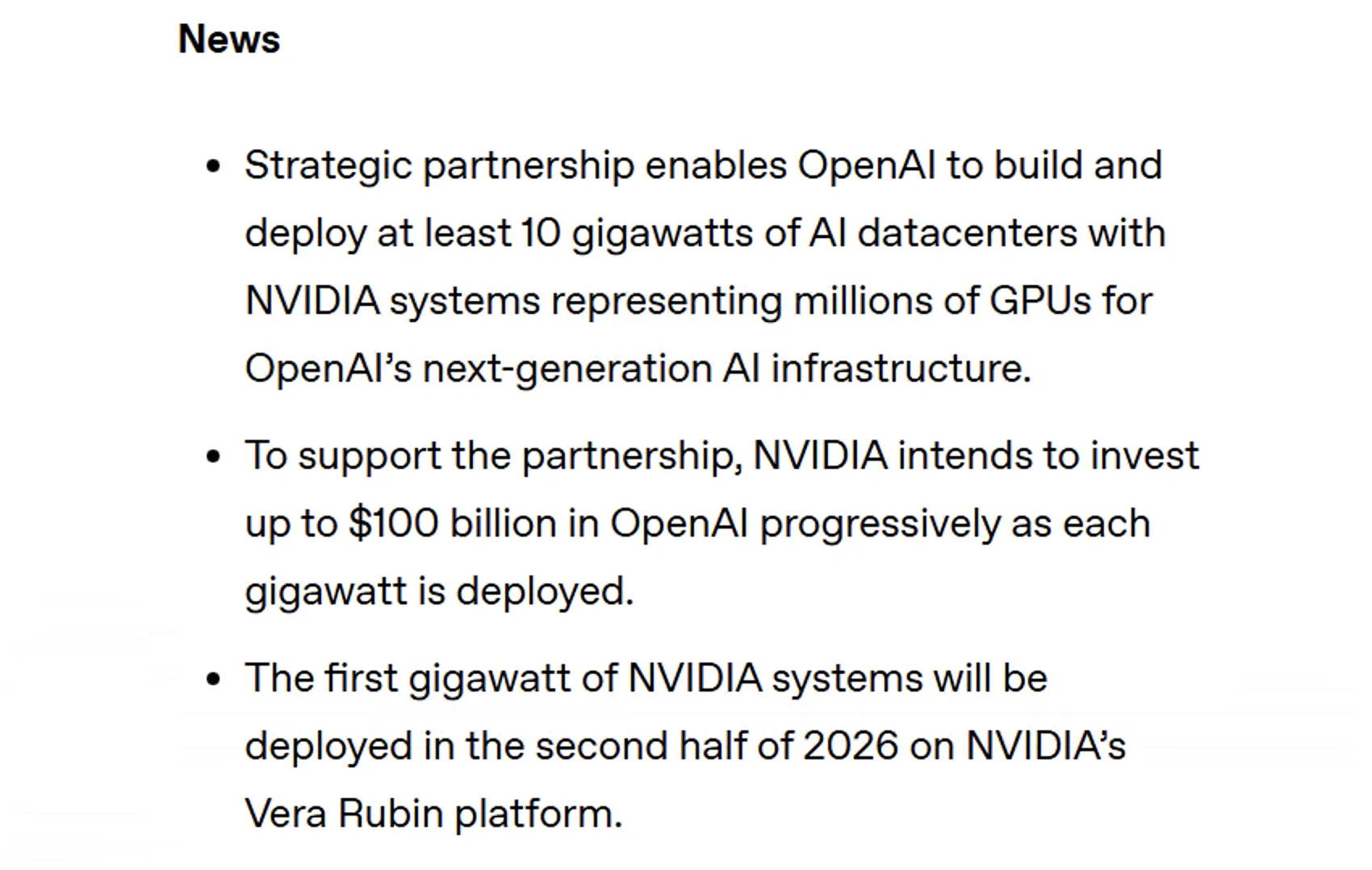

The partnership's technical details reveal the true scope of market manipulation at play. OpenAI and Nvidia plan to deploy at least 10 gigawatts of AI data centers—that's roughly equivalent to the power consumption of 7.5 million homes.

This isn't just about computational power. It's about creating infrastructure barriers so massive that no startup, regardless of innovation, can compete without begging for scraps from the table. When your AI model needs millions of GPUs to train effectively, and only one company controls the supply, you don't have a business—you have a dependency.

The shift from the original $100 billion commitment to $30 billion isn't retreat—it's precision targeting. Nvidia realized it didn't need to spend $100 billion to control the market. Thirty billion buys the same outcome with better optics and less regulatory attention.

Oracle's involvement in the broader $500 billion Stargate project, alongside SoftBank and Microsoft, completes the picture. These aren't separate investments competing against each other—they're coordinated moves by the same ecosystem to ensure no outside player can access comparable infrastructure.

Why AI Startups Are Already Dead (They Just Don't Know It Yet)

The startup graveyard is filling faster than anyone wants to admit. Companies like Cognition AI ($9.8 billion valuation), Snorkel AI ($6.35 billion), and Inflection AI ($4 billion) represent the last generation of independent AI players with meaningful valuations.

But here's what their valuations don't show: infrastructure dependency. Every one of these companies relies on the same GPU supply chain, the same cloud providers, and increasingly, the same investment ecosystem that Nvidia and OpenAI control.

The market is experiencing what experts call "AI-driven consolidation." As one industry analyst noted, "As valuations are now more reasonable, there could be a significant increase in mergers and acquisitions in the software sector, as large technology and AI labs want to acquire data and workflows."

Translation: the big players are about to go shopping. And when Nvidia-backed OpenAI starts acquiring these "competitors," it won't look like monopolization—it'll look like market maturation.

The combined market capitalization of top-tier AI companies exceeds $1.2 trillion, but that number masks a troubling reality. Most of that value is concentrated among companies that are either directly or indirectly controlled by the same infrastructure providers.

The Antitrust Blind Spot That's Enabling Digital Feudalism

Regulators are fighting the last war while missing the current battle. Traditional antitrust frameworks focus on market share and consumer prices, but the AI consolidation playbook operates through infrastructure control and circular financing—areas where current regulations are blind.

The genius of the Nvidia-OpenAI structure is that it doesn't look like a monopoly. OpenAI appears independent. Nvidia appears to be just a supplier. The investment appears arms-length. But the result is the same as vertical integration without the legal vulnerabilities.

"Access to high-end compute isn't widely available, and that's a competitive moat."

Antitrust concerns are emerging, but slowly. The closed ecosystem raises questions about market concentration and fair competition, but by the time regulators catch up, the infrastructure advantages will be insurmountable.

Meanwhile, investors are already rotating out of "crowded AI and mega-cap trades," as evidenced by the tech-heavy Nasdaq experiencing downward pressure while the Dow Jones hits historic highs. This rotation isn't skepticism about AI's future—it's recognition that the AI market is becoming a two-player game.

What This Really Means for the Future of Innovation

The $30 billion OpenAI investment signals the end of the AI gold rush and the beginning of the AI empire period. Innovation isn't dead, but it's increasingly happening within rather than outside the established power structure.

For entrepreneurs, the playbook has changed. Success now requires either becoming so specialized that you're indispensable to the giants, or finding ways to build entirely new categories that don't depend on traditional AI infrastructure. The middle ground—building better AI products with conventional approaches—is disappearing.

For investors, the consolidation creates opportunities in adjacent markets. As AI infrastructure becomes monopolized, the real returns will come from companies that can leverage AI without being captured by it. Think AI-enabled manufacturing, healthcare applications, or financial services that use AI as a tool rather than as their core product.

The fundamental question isn't whether artificial general intelligence will arrive—it's whether it will be controlled by a handful of companies or distributed across a competitive marketplace. The $30 billion OpenAI deal suggests we're rapidly approaching a future where the most transformative technology in human history is owned by the fewest companies in tech history.

The arms race isn't reaching a breaking point. It's reaching a conclusion. And the winners are already writing the rules for what comes next.