This $0.44 Canadian Gold Miner Could Hit $4+ as Major Buyout Targets Circle

First Mining Gold's $3.2B Springpole project sits in Agnico Eagle's backyard with environmental approval coming in 2026.

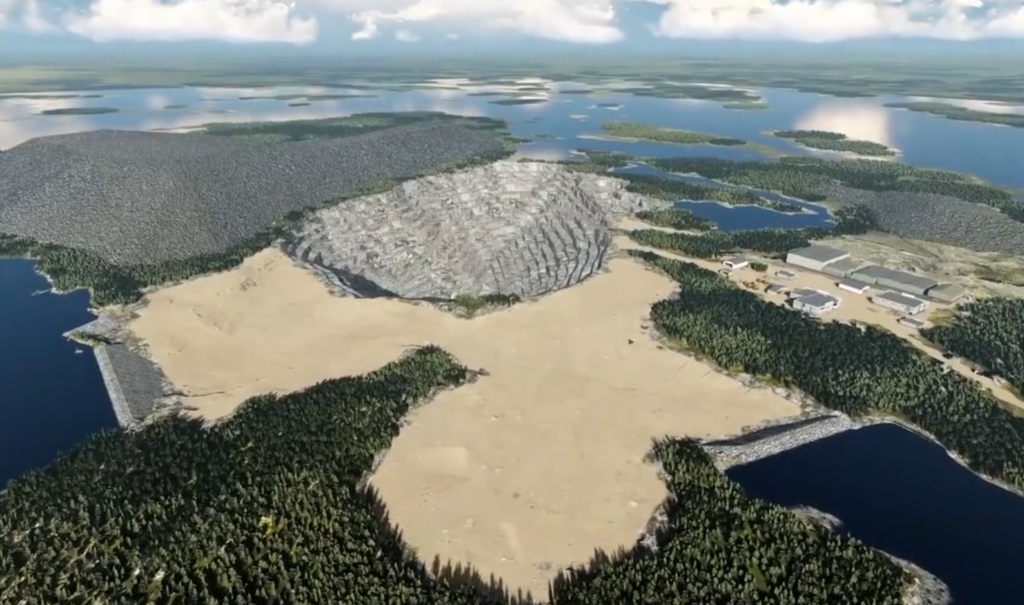

While gold stocks have rallied 23% this year, one Canadian gold miner trading at just $0.44 per share holds what might be the most undervalued asset in North America. First Mining Gold Corp (OTCQX: FFMGF) owns the Springpole Gold Project in Ontario, a 5-million-ounce deposit that just received a stunning $3.2 billion pre-tax NPV in its November 2024 pre-feasibility study.

The math is simple but striking. At current market cap of roughly $200 million, First Mining trades at just $40 per ounce of gold resources. Meanwhile, comparable Canadian gold miners trade at $150-200 per ounce. That valuation gap could close rapidly as environmental approval approaches in early 2026.

The $3.2 Billion Springpole Catalyst

First Mining's November 2024 pre-feasibility study revealed numbers that sent the stock up 35.8% in a single day. The Springpole project shows a $3.2 billion pre-tax NPV at current gold prices, with an internal rate of return exceeding 20%. Production would average 347,000 ounces annually over a 13-year mine life.

These aren't pie-in-the-sky projections. Ausenco Engineering, the same firm behind feasibility studies for major producers like Agnico Eagle, prepared the technical report. The study incorporates advanced metallurgical testing and updated engineering designs that reduced capital costs while improving recovery rates.

The project sits in northwestern Ontario, 110 kilometers northeast of Red Lake, in the heart of Canada's most prolific gold-producing region. Agnico Eagle's Macassa mine lies just 40 kilometers away, while the company's Red Lake complex dominates the broader district.

Environmental Approval: The Make-or-Break Moment

The single most important catalyst for First Mining Gold lies in environmental approval, expected in early 2026. The company submitted its Final Environmental Impact Statement and Environmental Assessment in November 2024 after years of consultation with Indigenous communities and regulators.

This isn't just another permit application. The environmental assessment process represents the final major hurdle before construction can begin. Success here would transform Springpole from a development project into a shovel-ready gold mine worth billions.

The convergence of sustained elevated gold prices and acute scarcity of advanced, permitted large-scale projects in stable jurisdictions creates exceptional value for shareholders.

First Mining has spent considerable effort building relationships with local First Nations communities. The socio-economic analysis shows Springpole would inject $15 billion into the Canadian economy over its mine life, creating thousands of jobs in northwestern Ontario.

Environmental concerns around the project center on Springpole Lake itself, where the open-pit mine would be located. However, comparative analysis shows the project would affect just 6% of the host lake, compared to 36% and over 70% for similar developments at Meadowbank and Gahcho Kué respectively.

Major Miners Circle Their Prey

Gold mining companies desperately need new projects. Global gold production has stagnated while reserves deplete, forcing majors to look at acquisition targets. Springpole's size, location, and advanced development stage make it an obvious target.

Agnico Eagle represents the most logical acquirer. The company already dominates the Red Lake district and has publicly stated its interest in growing reserves through acquisition. Adding Springpole's 5 million ounces would extend Agnico's regional dominance for decades.

Barrick Gold also fits the profile. The world's second-largest gold producer has been actively acquiring development-stage projects, particularly in stable jurisdictions like Canada. Springpole's scale aligns with Barrick's preference for tier-one assets.

The numbers suggest a buyout premium of 300-500% over current share prices wouldn't be unreasonable. Major gold producers regularly pay $150-200 per ounce for advanced development projects. Applied to Springpole's 5 million ounces, that implies a total project value of $750 million to $1 billion, compared to First Mining's current $200 million market cap.

The Path to $4+ Per Share

Several catalysts could drive First Mining's share price from $0.44 to $4+ over the next 18 months. Environmental approval represents the primary catalyst, likely adding $1-2 per share as construction risk disappears.

Strategic partnerships offer another pathway to higher valuations. Major miners increasingly prefer joint ventures over outright acquisitions, allowing them to share development costs while securing future production. A 50% partnership at fair value could immediately re-rate the stock.

The company has prepared for growth with a $500 million Canadian shelf prospectus filed in 2024. This gives management flexibility to raise capital quickly when opportunities arise, whether for project development or strategic acquisitions.

Gold price momentum provides additional upside. At $2,650+ per ounce, gold has broken to new all-time highs driven by central bank buying and geopolitical tensions. Higher gold prices directly improve Springpole's economics, with each $100 increase adding roughly $400 million to project NPV.

Risk Factors Every Investor Must Know

Environmental approval remains the biggest risk. While First Mining has invested heavily in community relations and environmental studies, regulators could still reject or significantly delay the project. This binary outcome explains much of the current valuation discount.

Financing represents another challenge. Springpole requires roughly $1.1 billion in capital expenditure, far exceeding First Mining's current market cap. The company will need equity raises, debt financing, or strategic partnerships to fund development.

Operational risks include cost inflation, construction delays, and metallurgical challenges. While the pre-feasibility study provides confidence, actual mining often reveals unexpected complications that increase costs or reduce production.

Regulatory changes in Ontario could impact the project's economics. Changes to mining taxes, environmental regulations, or Indigenous consultation requirements could delay development or increase costs.

The Investment Thesis

First Mining Gold offers one of the clearest asymmetric risk-reward profiles in junior gold mining. The downside appears limited given the company's cash position and asset quality, while upside could exceed 1000% if environmental approval triggers a buyout.

The stock trades at a massive discount to comparable development projects, offering patient investors exceptional value. With gold prices at record highs and major miners desperate for new reserves, the stars align for a significant re-rating.

At $30 per ounce versus peer average of $150-200 per ounce, First Mining trades at one of the deepest discounts in the sector.

Environmental approval in early 2026 represents the key catalyst that could unlock billions in shareholder value. Until then, First Mining remains a high-risk, high-reward speculation suitable only for investors comfortable with binary outcomes.

For those willing to accept the risks, First Mining Gold offers a rare opportunity to buy into a tier-one gold project at junior miner prices. The potential for 10x returns exists, but only for investors with strong conviction and patient capital.